The basic difference between standard and actual WIP calculations is basing the costs on quantities or time booked

WIP@Standard: Value of Actual Material Issued, Actual Sub con Issued, plus value of parts produced

(i.e. for each operation [(actual qty booked / planned qty) x total planned cost of operation])

WIP@Actual: Value of Actual Material Issued, Actual Sub con Issued, plus value of actual time booked

(i.e. for each operation [(actual hours booked / planned hours) x total planned cost of operation])

Both of these calculations are then apportioned to compensate for the fact that some of parts may be finished and WO Receipted.

i.e. the calculated value is multiplied by (WO Qty Received / WO Qty)

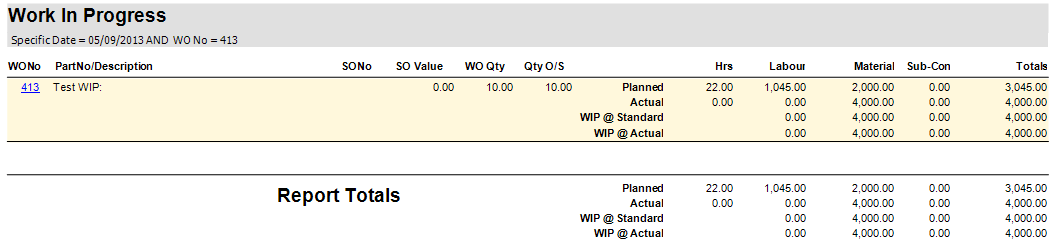

In the example below for WO 413:

There is half of the planned material issued to it, hence the WIP@Standard and WIP@Actual both represent £2000 which is only material.

=================================================================================

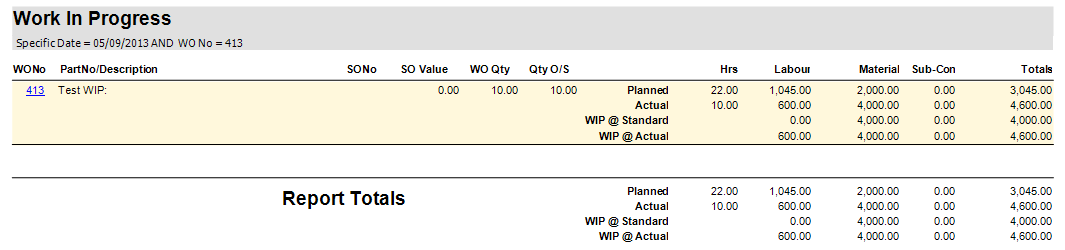

There has then been a labour booking of 10 hours against the first operation, but no quantities booked.

This cost is then attributed to the Actual labour WIP cost which is based on hours, but not the Standard which is based on quantities booked.

@Standard: of each operation, Actual Qty booked (0)/planned Qty (10)*total planned cost of op (660) = 0

@Actual: of each operation, Actual Hours booked (10)/planned hours (11)*total planned cost of op (660) = 600

====================================================================================

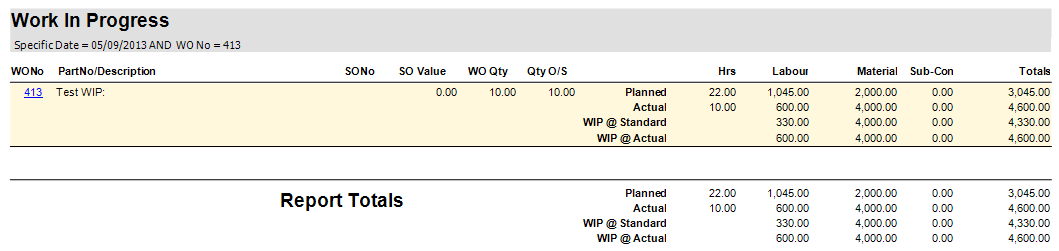

If a quantity of 5 is then added to the same clocking :

This will not change the WIP@Actual, but values are now entered against the WIP@Standard.

@Standard: of each operation, Actual Qty booked (5)/planned Qty (10)*total planned cost of op (660) = £330

@Actual: of each operation, Actual Hours booked (10)/planned hours (11)*total planned cost of op (660) = £600

=================================================================================

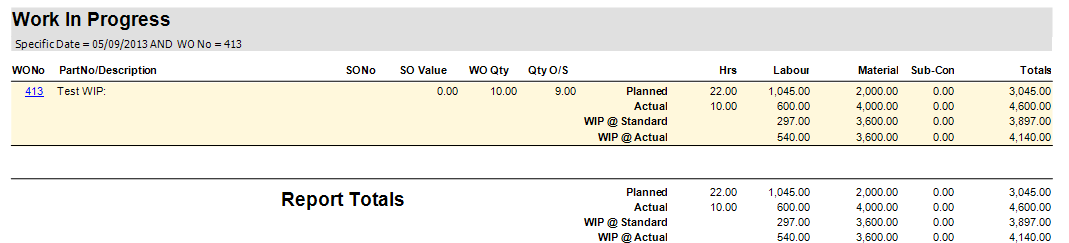

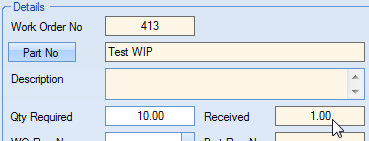

WO Quantities Receipted:

At this time there has been no quantities receipted against the WO, so if quantities are received the costs are prorate.

For example, when a quantity of 1 is received:

The planned and actual costs remain the same, but the WIP values change as follows:

| Labour @Standard: | calculated value (330) x (WO Qty Received (1) / WO Qty (10)) = £297 |

| Material @Standard: | calculated value (4000) x (WO Qty Received (1)/WO Qty (10)) = £3600 |

| Labour @Actual: | calculated value (600) x (WO Qty Received (1) / WO Qty (10)) = £540 |

| Material @Actual: | calculated value (4000) x (WO Qty Received (1) / WO Qty (10)) = £3600 |